For years, personalization in wealth management has been framed as an investment challenge.

How do we build better models? Can we customize portfolios without blowing up tracking error? How do we optimize taxes, factors, ESG constraints, or client-specific preferences at scale?

Those are important questions. But they are not the real bottleneck.

The truth is simpler and more uncomfortable:

Personalization is not primarily an investment problem. It is a workflow problem.

And until firms address it as such, personalization will remain something they talk about more than something they actually deliver.

The Illusion of the Investment Bottleneck

Most investment teams already have what they need to personalize portfolios.

They have:

- Capital market assumptions

- Factor models and risk frameworks

- Model portfolios

- Tax-aware logic

- Clear views on asset allocation and portfolio construction

In other words, the intellectual capital already exists.

What breaks down is not the idea of personalization. It is the execution of personalization inside real-world operating constraints.

Where Personalization Actually Fails in an RIA

When firms attempt to personalize portfolios at scale, the same issues show up every time:

- Advisors are forced to choose between standardized models or one-off custom portfolios

- Investment teams lose visibility once portfolios splinter into exceptions

- Operations teams drown in manual workflows, spreadsheets, and trade overrides

- Tax optimization becomes episodic instead of systematic

- Customization decisions live in people’s heads instead of systems

The result of all this chaos is predictable. Personalization becomes expensive to maintain and impossible to scale.

When that happens, firms ultimately retreat to model uniformity, while still marketing “customized solutions.”

Why Personalization Is a Workflow Problem for Advisors

True personalization is not about creating more models. I think every portfolio manager out there likely agrees with that.

Instead, personalization is about designing repeatable workflows that allow variation without creating chaos.

In practice, a workflow-centric approach to personalization looks like:

- Defining where customization is allowed

- Encoding constraints directly into portfolio logic

- Automating decisions that do not require human judgment

- Preserving investment governance while enabling flexibility

Personalization fails when it lives outside the system, but it works when it is embedded inside the workflow.

The Missing Layer: A Portfolio Operating Infrastructure

Here’s where the rubber really meets the road. Most wealth platforms for advisors have been built to accommodate one of two worlds:

| Centralized models with minimal deviation, OR… | Fully bespoke portfolios managed one at a time |

Neither world supports scalable personalization and neither fully addresses the way most advisor firms like to work when it comes to creating investment strategies and managing client portfolios.

What is missing for RIAs is a portfolio operating layer that can provide these four key supporting pillars:

- Support thousands of portfolios with shared DNA

- Allow controlled, rules-based deviations

- Optimize taxes, transitions, and rebalancing continuously

- Coordinate across accounts, sleeves, and households

Clearly, you can see that we aren’t dealing with investment engine problem. We’re dealing with a problem in how the entire system is designed.

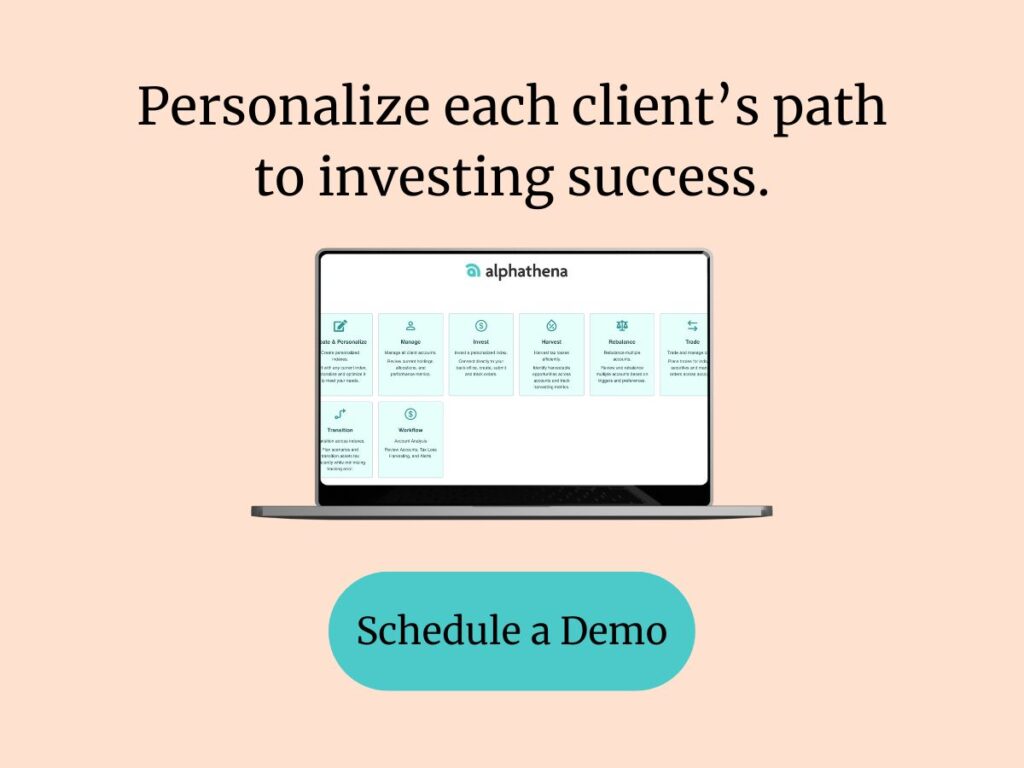

Alphathena’s View: Personalization as an Operating System

At Alphathena, we started building personalized investing from a different premise than the legacy tools that have been on the market. We started off with the assumption that investment teams already know what they want portfolios to do. Designing a platform that enables how that can be delivered at scale is the challenge.

That starting position led us to build personalization as a workflow-native capability:

- Direct indexing that supports both long-only and long/short strategies

- Sleeve-level and household-level portfolio management

- Systematic tax-loss harvesting and rebalancing embedded into daily workflows

- Transition analysis that models tax impact and tracking error before trades are placed

- Open architecture that integrates with custodians and downstream systems

For us, personalization is the default mode of operation, just like it is for your advisory firm in your day-to-day engagement with hundreds or thousands of unique individuals that you serve.

From “Custom” to “Configurable”

One of the biggest mindset shifts firms must make is moving from custom to configurable.

| Custom implies… | Configurable implies… |

| Manual work | Rules |

| One-off decisions | Guardrails |

| Operational risk | Repeatability |

Now, before we go further let’s address one thing: The goal is not infinite flexibility. That’s not a sustainable goal either.

The goal is controlled flexibility, delivered through software, so you can actually scale personalization throughout all the households your firm serves.

What This Means for Investment Teams

Four positives benefits emerge when personalization is treated as a workflow problem:

- Investment teams regain governance and visibility

- Advisors get flexibility without improvisation

- Operations teams reduce manual overhead

- Tax optimization becomes continuous instead of reactive

Most importantly, firms no longer have to choose between efficiency and personalization, because they can achieve both at once.

The Bottom Line

If your personalized investing strategy depends on single-person heroics, spreadsheets, or managing dozens or hundreds of exceptions, it will not scale.

If it depends on building ever more complex investment models until there’s no end in sight, you are trying to solve the wrong problem.

Personalization succeeds when it is engineered into the workflow itself.

That is the shift Alphathena is enabling, and it is why the future of personalization will be won by platforms that think like operating systems, not model marketplaces.