The wealth management industry is sitting on a $13.7 trillion managed account ecosystem1 that, for all its sophistication, still relies on a decades-old division of labor: advisors advise, and third parties manage portfolios using antiquated systems to integrate with custodians. Turnkey Asset Management Platforms and outsourced Separately Managed Account providers have built enormous businesses on this premise, collectively overseeing trillions in assets and charging 30 to 50 basis points2 for the privilege of handling the operational heavy lifting that advisors would rather not touch.

That arrangement made sense when the alternative was hiring an army of portfolio managers, analysts, and technologists to handle rebalancing, tax-loss harvesting, cash deployment, trade reconciliation, custodian integration, and the countless micro-decisions that keep portfolios aligned with investment policy. The economics were simple: outsource or staff up. Most firms chose to outsource.

But a new category of technology is rewriting this calculus. Agentic AI workflows are reasoning systems that can analyze portfolio situations, formulate plans, stage actions, and explain their reasonings. They do not make investment decisions. The advisor, PM, or analyst retains that authority entirely. What agents do is help those professionals do more, do it faster, and scale their expertise across far more accounts than was previously possible – enabled by a virtual team of portfolio manager, analyst, and technologist AI agents.

The implications for the TAMP and SMA outsourcing model are worth examining closely.

Video description: The Athena AI Agent for portfolio transitions.

Where the Money Goes

The SMA market has exploded in the last decade. Industry assets in managed accounts reached $13.7 trillion in 2024, growing nearly 20% year-over-year. SMA programs alone attracted $218.4 billion3 in net flows that year, the highest among all managed account types. Over five years, SMA programs have demonstrated a compound annual growth rate of 18.3% in assets under administration. Direct indexing closed 2024 at $864.3 billion in assets and were on target to to cross $1 trillion by the end of 2025.4 Cerulli research projects total managed account assets to reach $21.8 trillion by 2028.5

These numbers reflect massive demand for personalized, tax-efficient portfolio management. But they also mask a structural dependency. When an advisor allocates a client’s assets to a TAMP or third-party SMA manager, they are not just outsourcing the entire operational backbone: daily monitoring, drift detection, rebalancing, tax-loss harvesting, withdrawal processing, cash deployment, and trade reconciliation, each of which require dedicated PMs and analysts with deep operational expertise. They are also outsourcing their entire investment philosophy

For a mid-sized RIA managing $500 million, outsourcing to a TAMP at 35 basis points costs roughly $1.75 million annually. That buys operational convenience but not investment alpha. Most TAMPs implement the same models, the same rebalancing logic, and the same tax management rules across thousands of accounts. The value is in the execution infrastructure, not in proprietary insight.

Closing the Gap Between Platform and User

An agentic workflow is a system where AI does not just respond to queries, or step through an algorithmic workflow. It analyzes situations, formulates multi-step plans, stages actions, and explains its reasoning. In portfolio management, an agent can examine an account’s holdings, incorporate household nuances, evaluate its tax position, compare it against a target model, identify the constraints involved in a transition, and stage specific scenarios for the advisor to review, all without the advisor needing to understand the underlying optimization mechanics.

This is different from the automation that exists today. Current platforms offer powerful optimizers and rebalancing engines, but they require users to understand the knobs to turn and the trade-offs embedded in each configuration. The “fifth generation” of SMAs is characterized by mass customization enabled by algorithmic automation,6 but the gap between what platforms can do and what most users can extract from them remains enormous. That gap creates the need for dedicated portfolio analysts, or for outsourcing entirely.

Agentic workflows close this gap. They translate the advisor’s plain-language objectives into precisely tuned optimization parameters. The advisor states what they want to achieve. The agent configures how to achieve it. The advisor reviews, approves, or overrides. Investment judgment stays with the human at every step, and results are immediately available to iterate over

Do Not Sacrifice Effectiveness at the Altar of Efficiency

There is a temptation to evaluate agentic AI solely on what it does: the scenarios it builds, the trades it stages. But the most valuable capability agents bring to portfolio management may be the interpretation of the activity’s output.

Consider what actually consumes a portfolio manager’s day. A complex set of rebalancing or tax-loss harvesting actions across a book of business can take a full day, sometimes multiple days, for a PM or analyst to complete. The time is not spent solely on running the optimization. Much of it goes in reviewing results, validating that outputs align with client objectives, spotting anomalies, and making judgment calls about edge cases. The review and approval cycle creates the bottleneck, not the computation. When these tasks are outsourced, you are at the behest of an assembly-line process crafted to maximize efficiency, not effectiveness.

How Agentic Workflows Compress Review Cycles

Agentic workflows compress this cycle in two ways. First, the agent draws the user’s attention to the areas that need it. Instead of scanning hundreds of accounts for the handful that require a closer look, the PM sees a curated view: accounts where the rebalancing output produced an unexpected result, tax lots approaching a long-term holding threshold, positions where a wash-sale window conflicts with a harvesting opportunity. The vanilla outcomes move through swiftly with a confirmation rather than a full manual review.

Second, the agent interprets the output in context. It explains why a particular rebalancing produced a larger-than-expected trade list, what constraint was binding, which client restriction created a deviation from the model, and what the downstream tax implications look like. The PM is no longer building up from raw data to a conclusion. They are starting from an interpreted, explained result and deciding whether to accept, modify, or override it. The investment decision remains theirs. The agent just made the path to that decision dramatically faster and less prone to error.

This is the true value agents bring into the equation – maximizing both efficiency and effectiveness. Interpretation of the activity output to make decisions faster is as useful, if not more useful, than any other efficiency gains agents can provide.

Evolution from Robo-Advisor to Agent-Advisor

Robo-advisors are algorithmic rule-based execution engines. They apply a uniform strategy consistently across thousands of accounts: set the allocation, define the rebalancing bands, specify the thresholds, and the robot executes repeatedly at scale.

But robo-advisors cannot reason. They cannot look at an account’s unique circumstances, a concentrated position with significant unrealized gains, employment-related trading restrictions, a household tax situation requiring coordination across accounts, and determine the best approach. They follow rules; they do not interpret context.

Agentic AI reasons. It examines each account independently, weighs the nuances, identifies edge cases, and generates tailored recommendations with explanations. When it encounters something unexpected, say, a portfolio with zero long-term gains where a gain-restricted transition effectively becomes a loss-only transition, it reasons through the implication, adjusts its approach, and explains what it discovered. But it does not execute. It stages, explains, makes recommendations, and enables the human to make better decisions, faster.

Why Advisors Outsource (and What Changes the Math)

As of 2024, 45% of financial advisors use separate accounts,7 and allocations to SMAs are expected to continue to increase. Yet only 18% of advisors use direct indexing, with 26% choosing not to despite having access, and 12% being entirely unaware of it.8

This is a capacity and complexity problem. Direct indexing and custom SMA strategies demand operational expertise that most advisory teams do not have in-house. Many advisors default to outsourcing not because they lack conviction in their own investment philosophy, but because the operational burden at scale is too high. The TAMP model thrives on this friction.

Agentic workflows attack it directly. When an agent can compress what takes a skilled analyst 30 to 60 minutes into under 5 minutes of scenario generation, with full explainability, the economics of insourcing shift. A firm managing $500 million that replaces its TAMP relationship with an AI-native platform could recapture a significant portion of $1.75 million in annual outsourcing costs. The agent does not replace the advisor’s investment judgment. It eliminates the operational friction and delay that forced the advisor to outsource that judgment’s implementation in the first place.

What This Looks Like in Practice

Every function below follows the same pattern: the agent identifies opportunities, interprets results, directs attention, and helps the PM or advisor move through the review cycle faster and with fewer errors. The advisor then makes the investment decisions.

Tax Transitions. A PM building a transition plan manually iterates through the optimizer over multiple iterations, tweaking each constraint, until the output looks right. The agent collapses this into a single pass: it identifies binding constraints across gains, wash-sales, position restrictions, and target weightings, then generates multiple scenarios with full explanations. When constraints interact in non-obvious ways, such as a gain cap that effectively turns the transition into a loss-only exercise, the agent surfaces that insight immediately. The PM decides which scenario(s) to execute.

Rebalancing. Real-world rebalancing is messier than drift bands suggest. An account that drifted from a large deposit behaves differently than one that drifted from sector rotation. A position two days from long-term status should not be sold for a minor adjustment. A household with three accounts needs coordinated rebalancing across aggregate exposure. The agent evaluates these layers simultaneously, flags positions nearing holding period thresholds, and surfaces household-level offsets that may eliminate unnecessary trades. The PM reviews a prioritized, explained set of actions rather than validating a raw trade list.

Tax-Loss Harvesting. The complexity is not in finding positions below cost basis. It is in evaluating each opportunity against wash-sale exposure across related accounts, replacement security fit against restrictions, and whether the harvested loss generates meaningful after-tax value or just purposeless turnover. The agent surfaces high-value opportunities, explains why specific losses were passed over, and the PM reviews a ranked set of recommendations rather than searching account by account.

Trade Reconciliation and Monitoring. Monitoring 200 accounts daily means distinguishing signal from noise. The agent transforms this into review-by-exception: it flags discrepancies above tolerance thresholds and presents a prioritized daily brief. The PM focuses on accounts that need attention. The rest are confirmed clean.

Athena AI: Starting with Tax Transitions

We are putting this philosophy into practice with the launch of Athena AI in Tax Transitions.

Our platform has always provided the full optimization capabilities for transitioning accounts between models, strategies, or indices. But leveraging those capabilities required a deep understanding of the optimizer’s parameters: which knobs to turn, by how much, and in what combination. Even our most experienced users encountered edge cases that demanded trial and error.

The Transition Agent processes the current holdings, the target model, and the user’s requirements (gain constraints, position restrictions, trade preferences) to generate specific, implementable scenarios. Each scenario is actionable: something the user can run to see concrete outcomes. The agent does not decide which scenario is best. It presents the options, explains the trade-offs, and the PM or advisor chooses.

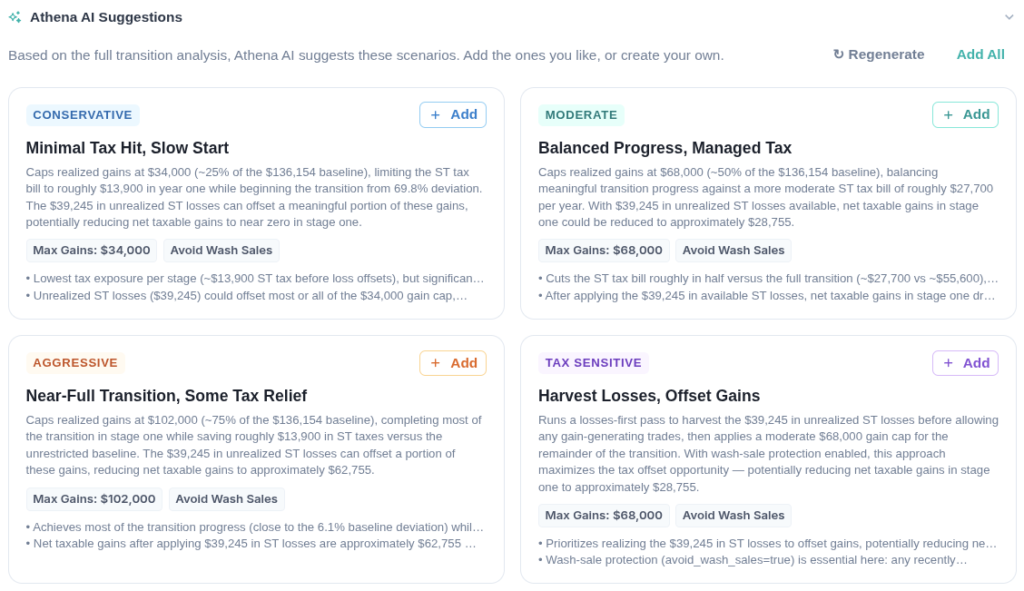

Image Description: Athena AI generates multiple transition scenarios, each with distinct tax and progress trade-offs, for an account being transitioned to a Direct Index.

An account with moderate unrealized gains needs to transition to a direct indexing strategy. An analyst would typically spend 30 to 60 minutes building scenarios manually. Athena AI does this in under a minute: conservative (minimize tax hit), moderate (balance progress with tax management), aggressive (complete most of the transition), and tax-sensitive (harvest losses to offset gains). Each includes a clear explanation of its construction and trade-offs.

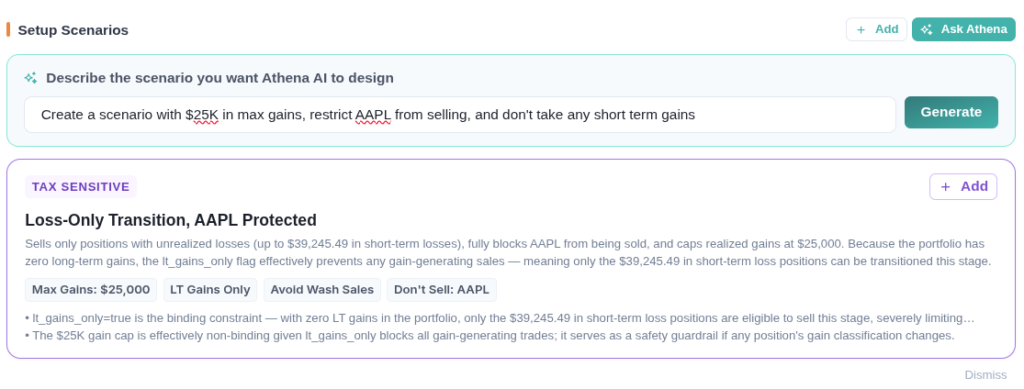

The real power emerges when users instruct the agent to build custom scenarios in plain language.

Image Description: A user requests a custom scenario. Athena AI reasons through the portfolio and identifies that the constraints effectively create a loss-only transition.

A user asks Athena AI to “create a scenario with $25K in max gains, restrict AAPL from selling, and no short-term gains”. The agent recognizes that with zero long-term gains in the portfolio, the long-term-only constraint combined with the gain cap blocks all gain-generating trades. The scenario becomes a loss-only transition. The agent explains the binding constraint and what is achievable. A well-versed analyst may reach the same conclusion, but likely not as quickly, comprehensively, or confidently.

The core optimization is still driven by our optimization engine. The agent translates intent into optimizer configuration and results back into human-readable insight. The investment math is deterministic. The agent does not make investment decisions. It makes the human faster, more informed, and able to scale their expertise across more accounts.

Beyond scenario generation, the agent explains the results of any transition in detail. A scenario produces dense output: capital drift, tracking error, realized gains and losses by holding period, tax impact, transaction counts, and multi-year forecasts. Connecting those numbers to each other and back to the constraints that produced them is real analytical work. The agent does it on demand.

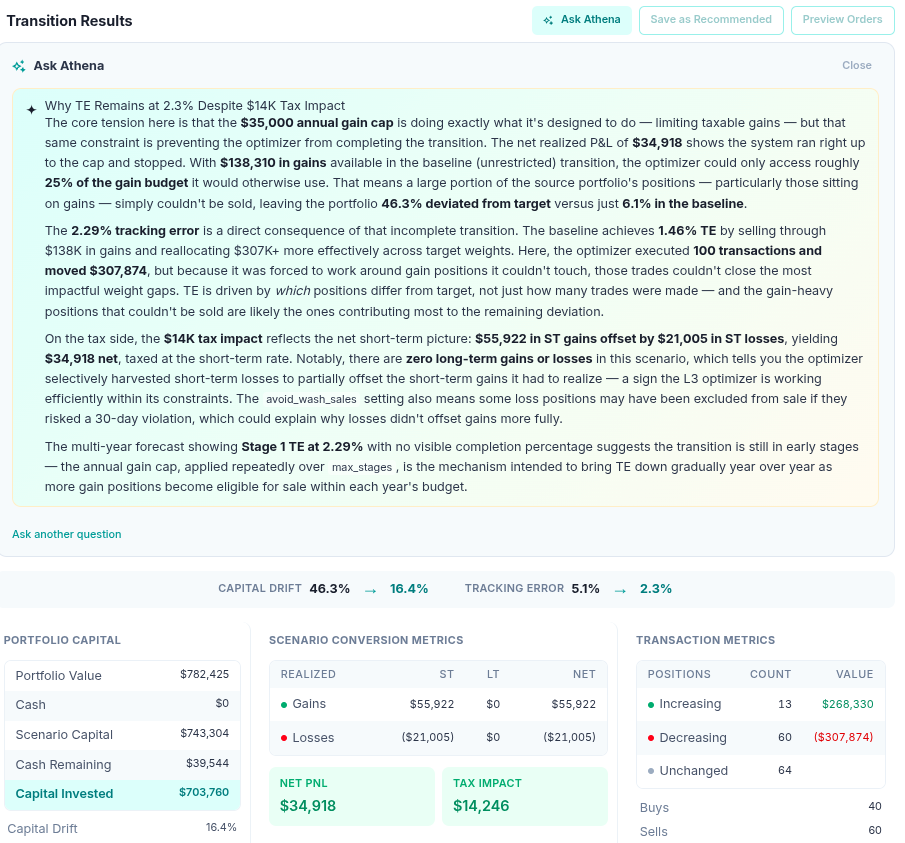

Image Description: A user asks why tracking error remains at 2.3% despite a $14K tax impact. Athena AI traces the answer through the gain cap constraint, capital drift composition, loss harvesting behavior, and the multi-year transition forecast.

In this example, the optimizer executed 100 transactions moving $307K in capital, realized $34,918 in net gains with a $14K tax impact, but left tracking error at 2.3% and capital drift at 16.4%.

The agent explains that the $35,000 annual gain cap is the binding constraint: with $138K in gains available in the baseline, the optimizer could only access roughly 25% of the gain budget. Gain-heavy positions sitting furthest from target could not be sold.

Tracking error is driven by which positions differ from target, not just how many trades were made, and the positions contributing most are precisely the ones the gain cap prevented the optimizer from touching. The agent traces through the loss harvesting behavior, the wash-sale avoidance implications, and the multi-year forecast showing how the transition is designed to play out over successive annual gain budgets.

A senior PM could produce this analysis, but the agent does it in seconds for any scenario.

What Makes an Agent Trustworthy

Deploying AI in portfolio management requires an exceptionally high trust bar. This is why we have built Athena AI around four non-negotiable principles:

Reliable. Consistent, accurate results grounded in actual portfolio data and optimization logic. No hallucinations. Every scenario can be implemented.

Repeatable. Identical inputs produce the identical outputs. No randomness, no drift.

Rational. The agent anticipates implications users might not see, like recognizing that a combination of constraints transforms a transition into a fundamentally different operation.

Readable. Every scenario includes a clear human-readable rationale: what constraints were binding, what trade-offs were made, what to pay attention to. An agent without readability is an agent nobody will use.

These are engineering requirements, not aspirations. AI that cannot be explained, verified, and trusted has no place in portfolio management.

Why Most AI-Only Firms Shy Away From Portfolio Management

AI adoption across wealth management is accelerating on many fronts. Meeting note summarization, CRM enrichment, growth marketing, client onboarding, and compliance documentation are all seeing meaningful agentic innovation, and for good reason. These applications deliver real productivity gains and solve genuine problems for advisors.

What is notable is how little of this innovation has reached the portfolio management workflow. The disparity reflects the structural reality that portfolio management demands a combination of prerequisites very few firms possess simultaneously.

Four Necessary Prerequisites

Deep domain expertise of the portfolio management process. An agent that participates in rebalancing, tax transitions, or loss harvesting needs to reason about tax lot accounting, wash-sale windows across related accounts, how corporate actions cascade through model targets, and the difference between a gain two weeks from long-term conversion and one that converted yesterday. This knowledge must be built by people who have lived inside the portfolio management process for years. General AI expertise alone does not get you there.

A deep, existing technology stack. The agent needs a production-grade optimization engine, real-time custodial connectivity, an order management system, a tax lot engine, model management, all built on top of a highly tailored, domain-specific, scalable and secure infrastructure. This is a multi-year engineering effort.

An agent without this foundation is a chatbot that talks about portfolios. It cannot manage one.

Zero tolerance for errors. A miscalculated wash-sale window means a client realizes a taxable event they did not authorize. A misread gain constraint generates an unexpected tax bill. Every output has to be verifiable, auditable, and correct.

Organizational agility to adopt AI fast. AI capabilities evolve on a timeline measured in months. Embedding agents into portfolio management requires teams that can iterate on constraint logic and user experience without 18 months of committee process. Large incumbents cannot move this fast. AI-focused startups often lack the domain and technical depth. The intersection of all four requirements is exceptionally narrow.

This is why more firms are building agents in tangential areas of wealth management than in portfolio management itself. It is not that those areas matter less. It is that portfolio management substantially raises the bar across every dimension. The firms that clear it will define the next generation of portfolio management technology.

The Insourcing Is Already Happening

The industry data tells part of the story. A significant number of RIAs are evaluating AI tools for various activities. 82% of platform sponsors identify improving tax management capabilities as a top priority.9 UMAs are on track to overtake rep-as-portfolio-manager programs as the largest platform type,10 creating the conditions for AI to be embedded deeply into portfolio management workflows.

But the more compelling evidence is what we are seeing on the ground. Advisors and home offices that were previously outsourcing complex portfolio management, including personalized direct indexing and active tax-loss harvesting, are bringing those capabilities in-house by adopting technology. These are not firms dipping a toe into basic model portfolios. They are running fully customized, tax-aware strategies with client-level personalizations. The cookie-cutter version of this was firmly in TAMP territory a few years ago. The exponential growth in assets under management on our platform, from firms ranging from boutique RIAs to large enterprises, is strong evidence that the appetite for insourcing is real and accelerating. These firms looked at the operational complexity that kept them outsourcing, concluded that the right technology could handle it, and made the move.

With over 15,870 registered investment advisers serving 68.4 million clients,11 each firm could have agents tuned to its investment philosophy, operational preferences, and compliance requirements. The agents adapt to the firm, not the other way around. The firms that lead this transition will rebuild workflows around what AI enables, treating agents as the foundational layer through which advisors interact with portfolio management, not as a feature bolted onto a legacy process.

What Comes Next

The Transition Agent is our starting point. We are launching with tax transitions because it is one of the most complex and underserved operations in portfolio management, where the gap between platform capability and user accessibility is widest.

The vision extends across the entire workflow: rebalancing, tax-loss harvesting, cash management, compliance monitoring, client reporting. Every function that currently requires deep optimizer expertise or outsourcing is a candidate for agentic augmentation.

The managed account industry is projected to reach $21.8 trillion by 2028.12 The question is not whether AI will transform how those assets are managed. It is whether incumbents will adapt fast enough, or whether a new generation of AI-native platforms will capture the opportunity. We believe the firms that embrace agentic workflows will deliver better outcomes, differentiate their practices, and scale without proportional increases in headcount, all while keeping investment decisions exactly where they belong: with the advisor.

Want to see Athena AI in action right now? Schedule a demo to take a platform tour.

References and Sources

- Cerulli Associates, “Managed Account Assets Reach $13.7 Trillion,” 2025. Reported via PLANSPONSOR. ↩︎

- TAMP platform fees typically range from 25 to 50+ basis points. Alphathena internal research.

↩︎ - Cerulli Associates, “The Cerulli Report—U.S. Managed Accounts 2025: Prioritizing Tax Optimization.” Reported via PLANSPONSOR, July 2025.

↩︎ - Cerulli Associates, “Direct Indexing Assets Close Year-End 2024 at $864.3 Billion,” The Cerulli Edge—U.S. Managed Accounts Edition, 1Q 2025. $1T projection: MMI-Cerulli Q1 2025 Advisory Solutions Data.

↩︎ - Cerulli Associates, “The Cerulli Report—U.S. Managed Accounts 2025.” Reported via PLANSPONSOR and InvestmentNews, July 2025. Projected annualized growth rate of 12.3%.

↩︎ - IKPMG, “Next-Generation SMAs Are Changing the Investment Landscape,” 2022.

↩︎ - Cerulli Associates, “In the U.S. Market, Conversions of SMAs to ETFs Are Growing,” The Cerulli Edge—U.S. Asset and Wealth Management Edition, April 2025.

↩︎ - Cerulli Associates, “Direct Indexing Assets Close Year-End 2024 at $864.3 Billion,” The Cerulli Edge—U.S. Managed Accounts Edition, 1Q 2025.

↩︎ - Cerulli Associates, “The Cerulli Report—U.S. Managed Accounts 2025.” Also: Cerulli / Parametric, “Customized at Scale,” 2025.

↩︎ - Cerulli Associates, “Managed Account Assets Reach $13.7 Trillion,” July 2025. Reported via PLANSPONSOR.

↩︎ - Investment Adviser Association / COMPLY, “2025 Investment Adviser Industry Snapshot,” May 2025.

↩︎ - Cerulli Associates, “The Cerulli Report—U.S. Managed Accounts 2025.” Reported via PLANSPONSOR and InvestmentNews, July 2025. Projected annualized growth rate of 12.3%.

↩︎